Construction Starts Falling Behind Needed Demand

July 22, 2024

Updated: May 20, 2026

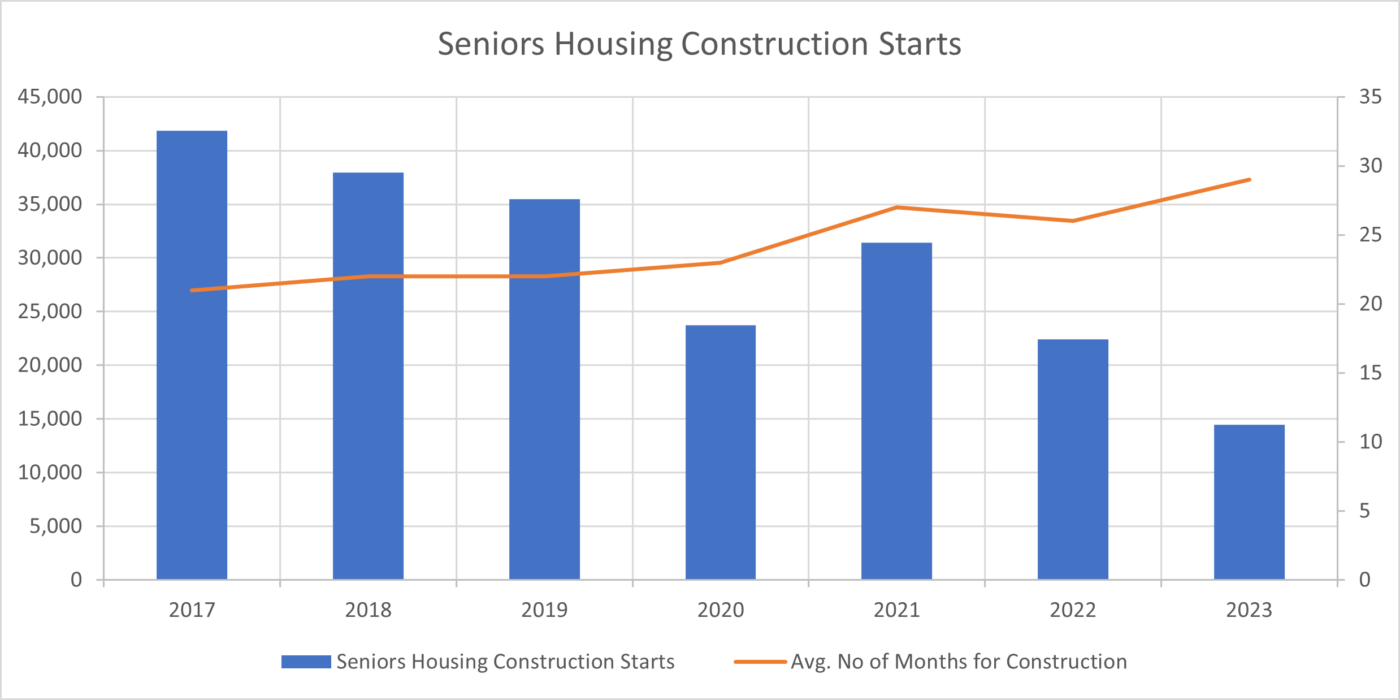

The landscape of senior housing has always been dynamic, reflecting the shifting demographics and evolving needs of an aging population. However, recent trends indicate a significant slowdown in senior housing construction starts, presenting a complex landscape of challenges and opportunities for operators, developers, and investors in the space. The chart below encapsulates the flux in new construction starts from 2017 through 2023, juxtaposed with the lengthening timelines of bringing these projects to fruition.

The State of Seniors Housing Starts:

In the wake of the global pandemic, the economic recovery has been uneven. Inflationary pressures, potential for recession, and heightened interest rates have made it difficult for developers and investors to forecast costs and returns, leading to hesitation in commencing new projects. Supply chain disruptions have significantly impacted the construction industry, causing material shortages and longer delivery times. A labor shortage, especially skilled labor in the construction industry, has led to increased labor costs and delays in project timelines.

In addition, to combat inflation, the Federal Reserve increased interest rates, which affects the borrowing costs for new construction projects. Higher financing costs can deter new developments, as they impact the overall profitability of long-term real estate investments. Due to this, banks and lenders have become more conservative in their lending practices for new construction projects due to the increased risk, thereby tightening the availability of capital. Furthermore, bank regulators have proposed new rules to materially increase a bank’s capital reserve requirement. Therefore, higher risk loans are becoming even more scrutinized and thus require even more capital reserves to protect against potential losses. While these regulations are not finalized, many financial institutions are already preparing as if they were.

All this combined has resulted in developers and investors dramatically slowing development at a critical time of high demand. New construction starts in 2023 were at a thirteen-year low of less than 15,000 units started. This is the lowest number of Seniors Housing construction starts since 2010, the year following the great financial crisis.

Extended Construction Timeline:

As the above chart demonstrates, not only have the construction starts declined, but the average number of months for construction has also seen a rising trend—from 21 months in 2017 to 29 months in 2023. This elongation of construction timelines, detailed in NIC MAP’s blog, Rising Construction Durations in Senior Housing: Beyond the Pandemic Effect, poses another challenging factor in meeting the expected demand of future seniors.

Where’s the Trough:

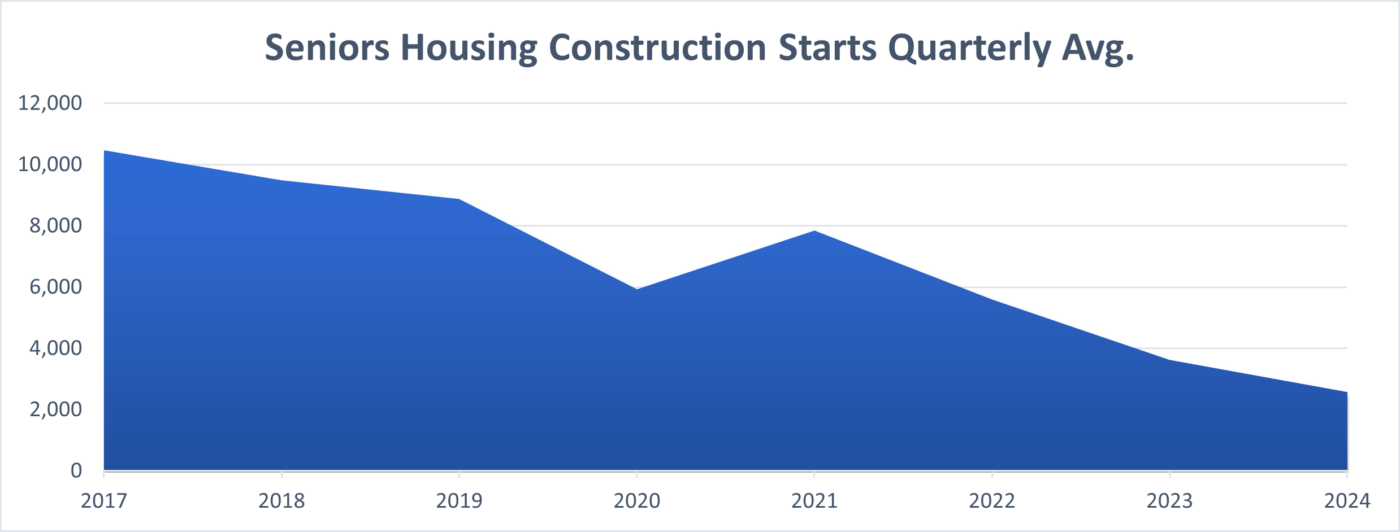

The trend of declining construction starts has continued into 2024 indicating 2023 was not the trough of this declining construction starts trend. Preliminary data from the second quarter of 2024 indicates that senior housing construction starts are averaging 2,579 starts per quarter this year, compared to a quarterly average of 3,617 in 2023. Preliminary estimates for the second quarter of 2024 were only 1,300 senior housing construction starts, which, even though subject to upward revision, is likely to be the lowest quarterly figure dating back to the quarters preceding the Great Financial Crisis.

What to Expect Going forward:

The historical decline in new construction starts, in 2022, 2023, and continuing into the first half of 2024 is a harbinger of a future pinch in inventory. The construction cycle in senior housing—from planning and approval to construction and eventual opening—often spans several years. Therefore, while the market may not feel the squeeze of today’s construction slowdown right away, the real impact is expected to ripple through the industry years down the line and will start to take effect as early as next year and worsen each year depending on how soon and how aggressively new development quickens.

This impending scarcity of new units will likely intensify competition for available spaces, likely leading to increased costs for residents. For operators, this forecasted gap underscores the need for strategic long-term planning and the exploration of innovative solutions to augment capacity, whether through expansions, renovations, or repositioning of existing assets.

Certainly, the intersection of high consumer demand and lack of new supply in senior housing is set to have profound effects on future seniors, investors, and operators in the industry.

For future seniors, the imbalance could lead to a lack of recently opened communities and potentially higher costs. As the baby boomer generation continues to enter retirement age, the demand for senior housing is only expected to escalate. However, if the construction of new facilities does not keep pace with this demand, seniors will find themselves competing for inventory, which can drive up prices and limit choices. This could exacerbate the issue of affordability for some seniors. Moreover, the lack of supply could lead to longer wait times for placement in preferred facilities, compelling seniors to consider alternative living arrangements or delaying the transition from one care level to the next.

Investors are seeing the supply-demand gap for what it is: a structural tailwind for the sector. Demographic demand keeps building, new supply keeps lagging, and existing senior housing assets sit on the right side of that imbalance. For capital already deployed in the space — and capital looking to deploy — the math gets more compelling, not less.

For operators, the current market dynamic reshapes the operating environment. Tight supply against strong demographic demand has historically corresponded with rising industry occupancy and supportive rent-growth conditions across commercial real estate. With fewer new facilities entering the pipeline, the existing operator base is serving a larger share of a growing addressable need — and the case for capital to flow into capacity expansion is getting stronger by the quarter.

In essence, the confluence of high demand and insufficient new supply is poised to create a tighter senior housing market, where strategic anticipation and operational excellence become critical differentiators for the various stakeholders involved.

Conclusion:

Based on the declining trend of new construction starts in 2023 and continuing in 2024, NIC MAP would anticipate a corresponding decrease in new inventory being delivered to market starting in 2025. Combined with consistent high demand, the senior housing market which has seen absorption chase inventory as a fallout of the pandemic, will quickly and profoundly switch to an industry where inventory is quickly chasing demand! Furthermore, this gap between high demand and decreasing new supply is likely to widen in the coming years depending on when capital becomes more readily available, and investors are ready to get aggressive on new construction.

As we continue to monitor these trends, we invite stakeholders to consider the urgent need for inventory and capital required to serve an aging population. To learn more about the $1 Trillion Requirement to Ensure Housing for All Seniors, read The Analysts Corner, The Impending Age Wave.