What 20 Years of Data Tell Us About the Future of Senior Housing

February 10, 2026

Updated: May 1, 2026

For two decades, the sector’s fundamentals have been quietly recording one of the most consequential long-term stories in U.S. real estate—and offering clear signals about the future of senior housing. Occupancy patterns, construction cycles, and consumer demand have moved through multiple economic environments—booms, recessions, capital surges, and capital pullbacks—yet the throughline has always been demand driven by demographics and need. As NIC MAP marks 20 years of data, the current moment stands out not because it is unprecedentedly volatile, but because the underlying fundamentals have aligned in a way the industry has not seen before.

Looking across 20 years of fourth-quarter snapshots from NIC MAP’s Primary Markets, two themes dominate the data: sustained demand growth and a structurally constrained development pipeline. Together, they define the senior housing environment today—and frame what lies ahead.

Twenty Years of Perspective Matters

NIC MAP began tracking senior housing and care fundamentals in Primary Markets in 2005, creating the industry’s most consistent, longitudinal dataset. Over time, that coverage expanded to include Secondary Markets in 2008—bringing insight across the top 99 metros—and an additional 40 markets in 2015. In 2026, as NIC MAP marks its 20-year data collection milestone, market coverage will expand again.

That long-term continuity matters. It allows today’s conditions to be evaluated not against short-term expectations, but against multiple cycles of development, capital availability, and demographic change. When viewed through that lens, the data points to a clear conclusion: demand has outpaced supply by a wider margin than at any other point in those 20 years.

Demand Has Evolved Beyond Prior Cycles

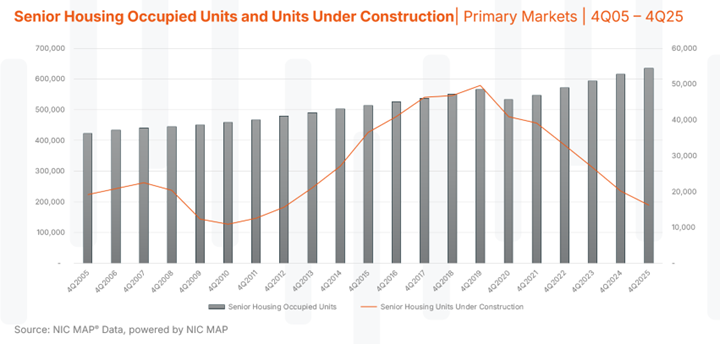

The chart below, which tracks occupied units alongside units under construction, shows a decisive shift. Occupied units today sit well above levels seen prior to 2020, underscoring how deeply embedded consumer demand for senior housing has become. This is not a temporary fluctuation. It reflects a new reality: more older adults are choosing—or requiring—professionally managed senior housing and care. That demand foundation is one of the clearest indicators on the future of senior housing.

What makes this moment distinct is not simply the level of demand, but its relationship with supply. The gap between growing occupied units and declining construction activity has never been wider in the 20-years of tracking during the aftermath of the 2008–2009 financial crisis, when development activity slowed sharply, the divergence was narrower than what the industry is experiencing today mainly because demand is so much higher than where it was nearly 20 years ago. That widening gap between demand and supply will play a defining role in the future of senior housing.

This gap speaks volumes. New development has not kept pace with senior demand, not because financing constraints, higher capital costs, and development hurdles have materially limited new starts. The result is a senior housing landscape where demand momentum is colliding with a restrained construction environment—an imbalance that reshapes market dynamics for the next decade.

Construction Cycles Have Changed

Historically, senior housing development responded relatively quickly to improving fundamentals. Periods of rising occupancy often encouraged new development, eventually leading to increased competition and moderation in performance. The current cycle has diverged from that pattern.

Units under construction have trended downward even as occupied units continue to rise. This is not indicative of a lack of confidence in senior housing as an asset class; rather, it reflects the realities of today’s capital markets. Development feasibility has become more challenging, extending the timeline for supply response and reinforcing the long-term importance of existing inventory.

From a macro perspective, this dynamic suggests that the industry is operating under a different supply regime than in prior cycles. When viewed across two decades of NIC MAP data, the nature of today’s construction slowdown becomes clear. How quickly—or slowly—new supply responds to demand will be central to the future of senior housing.

Senior Housing Occupancy Has Reached a New Plateau

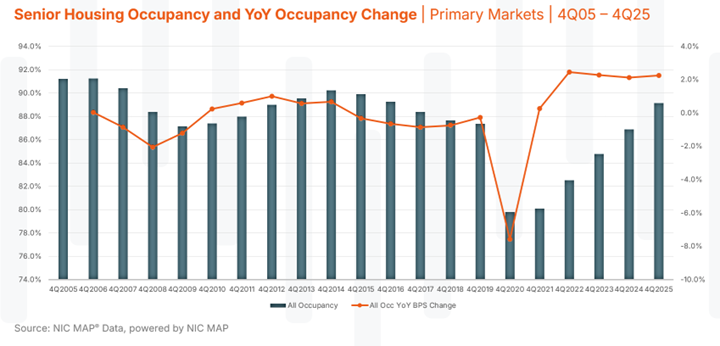

The chart below reinforces the strength of current fundamentals. Total senior housing occupancy now exceeds 89%, the highest level recorded since the end of 2016. More notable than the absolute level, however, is the trajectory that led here.

Over the past four consecutive years, the industry has recorded more than 200 basis points of occupancy growth each year. Four years ago, senior housing occupancy stood at 82.5%. Today, it is 89.1%. Sustaining that level of consistent, year-over-year growth across such a large and diverse set of Primary Markets is extraordinary by historical standards.

Across 20 years of NIC MAP data, no other annual change in occupancy included more than 200 basis points except for the last four years. Occupancy gains of this magnitude are typically uneven, interrupted by supply surges or shifts in demand. This cycle has been different. Growth has been steadily high, broad-based, and consistent.

What Sustained Occupancy Growth Signals

High and rising senior housing occupancy carries implications well beyond near-term performance metrics. It reflects deep-rooted consumer demand driven by aging demographics, longer life expectancy, and increasing care needs. It also reinforces the value proposition of senior housing as essential infrastructure within the broader healthcare and housing ecosystem.

Importantly, this growth has occurred without a corresponding surge in new development. That combination—strong occupancy alongside declining construction—reshapes competitive positioning, operating leverage, and long-term planning across the industry.

For operators, it underscores the importance of execution, staffing stability, and service quality in a demand-rich environment. For investors, it highlights the durability of senior housing fundamentals over full market cycles. For policymakers and planners, it raises questions about how future supply will be delivered as demographic pressure continues to build.

The Value of Longitudinal Data

One of the defining strengths of NIC MAP is the ability to contextualize today’s conditions within a 20-year historical framework. Short-term data can highlight movement; long-term data shows what will matter most for the future of senior housing. By consistently tracking senior housing occupancy, construction, and development activity across multiple economic eras, NIC MAP provides the industry with clarity that cannot be replicated elsewhere.

That perspective matters especially now. Without it, today’s supply-demand imbalance could be misread as cyclical rather than sustained. The data shows otherwise. When compared to prior periods, including the global financial crisis—today’s divergence between demand growth and new development stands apart.

Looking Ahead with Confidence and Clarity

Across 20 years of NIC MAP insight in the senior housing and care industry, the data reinforces what has consistently underpinned the sector: powerful demographic momentum paired with evolving lifestyle and support needs. An expanding older population, longer life expectancy, and increasing longevity have driven sustained utilization of senior housing, but the demand extends beyond clinical care alone. For many residents, particularly in Independent Living, the value proposition is rooted in access to community, social engagement, services, and housing designed for aging in place. Across economic cycles, these combined factors have translated into durable demand, underscoring why long-term fundamentals—not short-term market conditions—continue to shape the industry’s trajectory.

Senior housing has always been a long-term business, and the past two decades of NIC MAP data offer clarity into the future of senior housing. With market coverage expanding in 2026, NIC MAP will continue to provide the industry with the long-term perspective needed to understand where senior housing is headed.