Senior Housing Development Trends Point to a Growing Supply Constraint

Published Date: March 31, 2026

Senior housing construction trends are telling a very clear story. Development activity across the sector has slowed materially, with new inventory growth, active construction volume, and construction starts all trending down.

For an industry that depends on a steady pipeline of new communities to meet long-term demographic demand, the alignment of these indicators is significant. Data tracked by NIC MAP, which this year marks 20 years of providing senior housing and care analytics to the industry, shows that new development across both Independent Living and Assisted Living properties has slowed to levels not seen in over a decade.

Combined with accelerating demand, the data suggests that the sector is in a sustained period where supply growth cannot keep pace with the demographic demand forming ahead. The development cycle in senior housing is long, and the projects that are—or are not—starting today will shape the availability of new communities for years to come.

Inventory Growth Slows to a Rare Level Across Property Types

The first indication of this shift appears in the pace of new inventory growth. According to the most recent NIC MAP data release, annual inventory growth—measured as the net change in operational units—has fallen below 1% for three consecutive quarters. What makes this observation particularly notable is that the slowdown is occurring simultaneously across both Majority Independent Living (IL) and Majority Assisted Living (AL) properties.

Over two decades of industry tracking by NIC MAP, there has never been a period when both property types experienced inventory growth this slow at the same time. Over the long history of the sector, development cycles have often varied between property types. Today, however, the slowdown is broad-based.

Inventory growth at this level means that the sector is adding relatively few new units compared with its existing base of communities. From a development perspective, this metric represents the final stage of the construction pipeline. Inventory growth reflects the projects that were financed and started several years ago and are now at completion and opening to residents. When this metric slows, it often reflects conditions that began earlier in the development cycle.

Some Markets Are Now Seeing Inventory Declines

Looking more closely at market-level trends reveals another dimension of the slowdown. In several metropolitan markets tracked by NIC MAP, the total operational inventory of senior housing units has actually declined. This occurs when unit removals, whether from closures, disqualifications, or the consolidation of units within existing communities, exceed the number of newly opened units. Closures and repositioning are a normal part of the real estate cycle. Communities age, ownership strategies evolve, and properties occasionally transition to other uses. What is different in the current environment is that the development pipeline in some markets is not replacing those units at the same pace.

A broader look across the 140 markets covered by NIC MAP highlights how widespread this development slowdown has become. More than half of all coverage markets currently have no senior housing development projects underway at all. Another 20% of markets have only a single project under construction. At the other end of the spectrum, less than 10% of markets have four or more projects underway. This distribution shows how uneven the development pipeline has become. In many markets across the country, new senior housing construction activity is at best minimal, if not non-existent.

Construction Activity Near Cycle Lows

The slowdown in new inventory is closely tied to the volume of communities currently under construction. Across the sector, total units under construction are near cycle lows. This observation applies to both Majority IL and Majority AL properties, reinforcing that the slowdown is affecting the broader industry rather than a single product segment.

Construction activity represents the middle stage of the development pipeline. Communities under construction today are the ones expected to deliver new inventory over the next year or two. When construction volume declines, it signals that future inventory growth will remain limited.

The current development environment reflects several structural realities in the capital markets. Financing costs remain elevated relative to the previous decade, construction costs have increased, and developers are approaching new projects with greater selectivity. These conditions have contributed to fewer projects advancing from the planning phase into active construction.

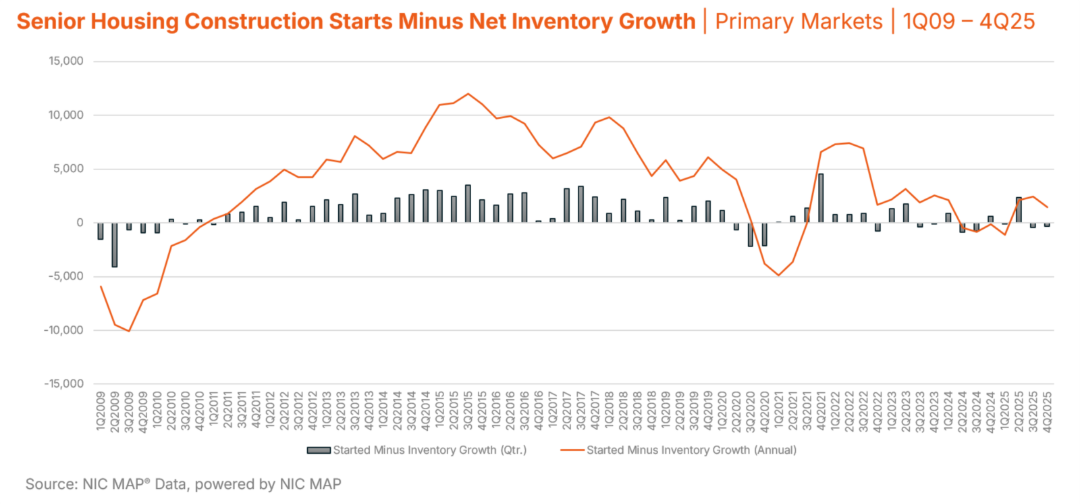

Construction Starts Fall to a Decade Low

Perhaps the most important signal comes from the earliest stage of the development cycle: construction starts. As a rolling four-quarter total, senior housing construction starts have declined to a decade low, according to NIC MAP data. This metric tracks the number of new senior housing units that are breaking ground, offering a forward-looking indicator of future supply.

What makes the current level of construction starts notable is how it compares with demand trends across the sector. Absorption—defined as the net increase in occupied units—has remained strong, indicating that demand for senior housing communities continues to grow.

When absorption and construction starts move in opposite directions, the imbalance becomes increasingly visible over

time. If construction starts remain at their current pace, the pipeline of communities expected to open later in the decade will remain limited. For an industry with a development cycle that can easily span two or more years from planning to completion, the slowdown in construction starts today has long-term implications for the availability of new communities in the years to follow.

Slow Starts Suggest Limited Inventory Growth Ahead

The relationship between construction starts and inventory growth is not immediate, but it is highly predictive. Because senior housing communities require significant time to plan, finance, and build, the level of construction starts today often determines the level of new inventory that will arrive several years from now. When construction starts fall, inventory growth slows in the years that follow.

Recent NIC MAP data shows that slow inventory growth is now mirroring the slowdown in construction starts. The alignment of these indicators suggests that new supply growth is likely to remain limited in the near term. This does not mean that development activity has stopped altogether. Projects continue to move forward in select markets where financing conditions and local demand dynamics support new construction. However, the overall pace of development across the national market remains constrained relative to historical levels.

A Structural Supply Gap Is Taking Shape

Taken together, the latest senior housing construction trends suggest the sector may be entering a period where supply growth struggles to keep pace with demand. Development activity has slowed materially, with new inventory growth, active construction volume, and construction starts all trending lower simultaneously. Because the senior housing development cycle can span several years—from planning and financing to construction and opening—today’s slowdown in construction starts will influence the availability of new communities well into the second half of the decade.

At the same time, demographic demand is beginning to accelerate as the oldest baby boomers approach their 80s. Absorption trends across the sector indicate that new residents continue to enter the market at an elevated pace compared to historical norms and at a steady pace in recent years, indicating a new benchmark for annual demand. When demand expands while new development remains limited, the result is tighter market conditions.

This dynamic is already setting the stage for a multi-year supply constraint. With relatively few communities currently under development across many markets, the industry will experience a period where new inventory growth remains limited while demand continues to build. In such an environment, industry occupancy will rise to historic levels, operators gain stronger pricing power, and margins can improve. These conditions can also support higher property valuations as capital markets respond to stronger operating performance across the sector.

Longer term, the implications for development are significant. Analysis presented in the NIC MAP Senior Housing Market Outlook suggests that maintaining balanced market conditions later this decade will require development activity approaching twice the historical pace of new construction. The scale of demographic demand forming in the coming years means that the next major development cycle will ultimately become the largest in the industry’s history.

Meeting that future demand will also require substantial capital investment. Projections highlighted in the outlook suggest that if development continues at its current pace, the sector could face a $275 billion supply gap by 2030, with the long-term capital required to expand senior housing inventory potentially exceeding $1 trillion by the early 2040s. For investors and developers, these projections highlight both the magnitude of the challenge ahead and the scale of opportunity that may emerge as the industry works to expand supply in line with demographic demand.

Looking Ahead

Development trends in senior housing often unfold slowly, but their long-term implications can be significant. The latest data from NIC MAP, now marking two decades of tracking senior housing development and market performance, shows a development pipeline that has slowed across nearly every stage—from construction starts to new inventory delivery.

For industry participants, these trends underscore the importance of understanding where development activity is occurring, where it is not, and how today’s construction decisions may shape the sector’s future supply. As the industry looks ahead to the next phase of demographic demand, the projects that begin construction today will determine how effectively the sector can meet the housing needs of tomorrow’s seniors. In that context, development activity across senior housing will remain one of the most important indicators to watch in the years ahead.